#22 Kooth: A public mental health business with software margins?

H1 Earnings Breakdown, comparison to public peers, a mega Cali contract and more

Hi friends,

Let’s get straight into it today. No messing around. There’s a mental health business from the UK that just delivered some serious financial results.

Check these out:

- £33m revenue (181% YoY growth)

- 82% Gross Margin

- £8m adjusted EBITDA

- £4m profit after tax

The company is called Kooth and they provide digital products to help improve young people’s mental health. Today, we dive into their business, analyse their H1 earnings and see what we can learn from them.

Improving youth mental health is a topic I care deeply about. In fact, I think it is the single most important issue facing our society. So I’m very excited to be discussing an organisation working on this problem.We’ll discuss;

- The Story of Kooth: There aren’t too many mental health tech companies that have been around for 23 years

- H1 Earnings Breakdown: 181% revenue growth + software margins

- Peer Review: How Kooth compares to other public mental health companies

- California Dreamin’: The mega-contract Kooth landed with California and how it could make or break them

- Expectations: Should we expect this growth and profitability to continue for Kooth

1. The story of Kooth:

If you don’t know about Kooth, here’s the quick background:

Who are they? A UK company providing digital products focused on prevention and early intervention for young people.

What is their product? A mobile app that has three main features; (1) a moderated community where young people can post anonymously, (2) content journeys, (3) access to counsellors for text based support

Who pays? Mainly government (California State, NHS etc.)

Kooth were founded way back in 2001 to tackle mental health prevalence in adolescents and have remained focused on that goal for the last 23 years. In 2020, they went public on the London Stock Exchange raising £26m at a valuation of £66m.

Kooth continued to work away quietly since their IPO, delivering on several NHS contracts in their home country of the UK. Revenue growth was moderate over this period, growing from a small base of £13m per year in 2020.

Gross margins were strong but Kooth was losing money each year. This put pressure on their cash reserves and shareholders took notice, with the share price dropping to £110 in October 2022 (a 55% decline from their IPO price).

But there was a big growth opportunity on the horizon for Kooth… the US of A!

In 2023, they landed a huge deal. A MEGA deal, if you will, with the state of California to deliver their platform to all young people in the state aged 13-25. To deliver on this plan, Kooth raised a £10 million round in Q3 2023, improving their cash position and allowing them to build the product and team that would be needed to deliver on their California contract.

Their product has remained focused on improving the mental health of young people through early intervention and prevention, with research showing they improvement for users in 70% of cases. From a health system perspective, they are focused on reducing demand for downstream acute mental health services and the costs associated with them.

In January of this year they launched their product in California (under the name Soluna) and started to roll it out with young people. They also started to recognise revenue from this deal and in last week’s H1 earnings release, we saw exactly the impact it has had on their P&L.

2. H1 Earnings Breakdown

Here are some of the highlights from Kooth’s H1 2024 earnings release.

𝐅𝐢𝐧𝐚𝐧𝐜𝐢𝐚𝐥 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬:

- Revenues up 179% to £32.5m

- ARR up 181% to £60m

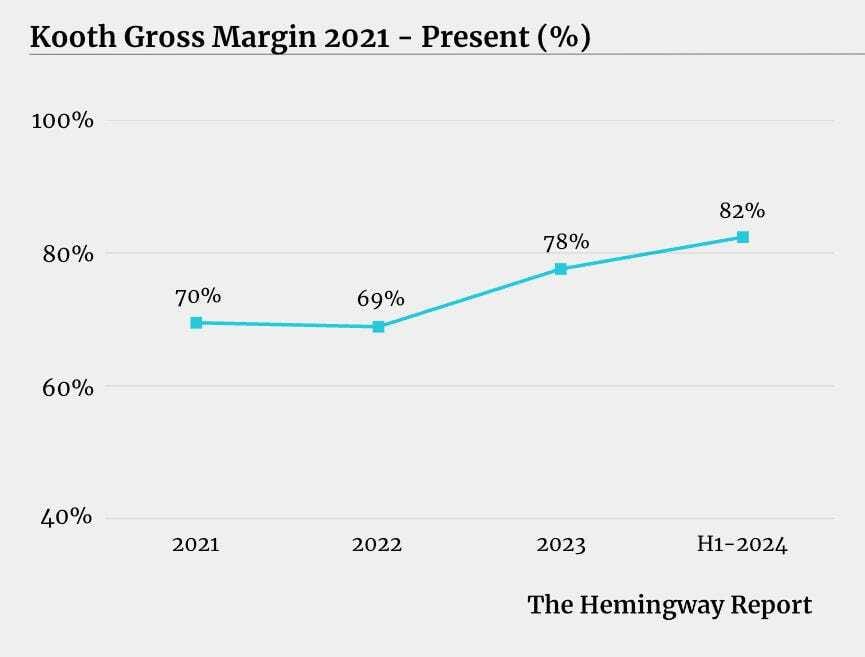

- Gross margin up 15.6ppt to 82% (Excuse me, what? A mental health business with >80% gross margins?)

- Adjusted EBITDA up to £7.8m

- Profit after tax of £3.9m

𝐈𝐦𝐩𝐚𝐜𝐭 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬:

- 70% of mental health coaching users reported positive outcomes from single-session therapy

- 95% would recommend Soluna to a friend

- 88% of students reporting they received the support they needed (for their service delivery in Pennsylvania)

- 53% of California based users come from communities disproportionately affected by health and economic inequities

𝐁𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬:

- US market now accounts for approximatley 70% of ARR

- Delivered first US private sector partnership with Aetna Better Health of Illinois

- Launched video based 1-2-1 coaching and care navigation support (I’m a huge fan of care navigation so was very glad to see this!)

Got questions? Me too. Let’s see if I can answer them for you.

How did they increase revenue by 179%?

Essentially, this all came from their California contract. This contract has a value of a whopping $188m over four years, starting in 2024. That is just a monster of a contract - but more on that (and its nuances) later.

As Kooth started to recognise revenue from this contract, their US Revenue increased to £23.3m in H1, compared to only £1.8m in H1 2023.

UK revenue was down 6% YoY however, driven by “an increase in churn in our English contracts being a combination of funding unavailable to continue pilot contracts, reductions as contracts consolidated and a single competitive loss“.

How did they achieve 82% gross margins?

The major challenge for most behavioral health businesses is trying to generate high enough gross margins to sustain the opex and investment required to build a business at scale.

In Q2 2024, Talkspace operated at a 45.5% gross margin - a number which has been declining over time - and many other players operate at similar levels.

But not Kooth…

How are Kooth delivering these software-like, 82% gross margins? And how are they increasing those margins over time?

Well, it’s because they actually are a software business.

While platforms like Talkspace, BetterHelp want to be viewed (and valued) as software businesses, they simply aren’t. They are software-enabled, service businesses and the proof is in their margin.

Kooth are different however.

While they do employ some practitioners to deliver care and monitor their platform, it is not their primary offering. Their primary offering is a digital product that users engage with to improve their mental wellbeing.

Software product = software margins.

Their model is based on helping most people get the support they need from “self directed or single-session therapy”. This allows them to deliver outcomes to populations at scale without having to build a massive workforce of practitioners.

As revenue has grown, their direct costs (the cost of practioners) has not scaled proportionately, allowing their margins to expand.

“We have seen an increase in gross margin driven by the US with the roll out of the Soluna app where we are initially seeing lower practitioner costs as contract usage ramps up and a greater use of the community and self guided tools. “

They only have 303 practitoners as of the end of H1 2024.

I was interested to see what sort of revenue they generate per-practitioner and compare it to Talkspace.

Here’s what I found…

Further proof that Kooth are not a service business, but a software business.

But that got me thinking, how do they compare to Talkspace (and their broader set of peers) on other metrics…

3. Peer Review

First let’s look at Gross Margin. Kooth has the highest Gross Margin amongst all their public peers, more than double that achieved by Lifestance.

However, they are MUCH smaller than most of their peers, only bringing in $43 million in revenue in H1 compared to Acadia’s $1.5bn.

But look at their growth, they’ve grown at 178% YoY, much faster than any of the other public companies in their peer set.

So how does that translate to their valuation multiple?

Essentially, they sit right in the middle of their peer set with an EV/Revenue multiple of 2, higher than the pureplay tech businesses like Teladoc and Talkspace but lower than behavioural health juggernauts operating brick and mortar operations like LifeStance and Acadia.

Considering their growth rate and margins, you could argue that Kooth are undervalued. But their small size, revenue concentration in a handful of large customers plus the uncertainty on future revenue sources is likely keeping their multiple in check.

Either way, it’s fascinating (at least for a nerd like me) to have a public mental health software business that we can analyse and compare to peers.

4. California Dreamin’

Kooth’s future hinges on their ability to expand in the US. And that ability relies on delivering positive results for their mega contract with the state of Claifornia.

This contract came about as part of California Governor Gavin Newsom's $4.7 billion investment in youth behavioural health, the Master Plan for Kids' Mental Health, and the Children and Youth Behavioral Health Initiative ("CYBHI").

In 2023, Kooth won the contract to deliver a platform for Young People aged 13-25, with Brightline responsible for the delivery of a service to 0-12 year olds.

As I mentioned, the contract is ginormous, with a value of $188m over four years. But perhaps even more valuable than this, is what a successful program with California would unlock for Kooth with other states and payers across the nation.

I’ve spent a lot of time thinking about companies like Kooth and seeing how others have succeeded and failed. And I can tell you this with certainty, the fate of this contract will come down to two things; their ability to get young people to use the product and their ability to deliver (and prove) outcomes?

1. Can they get young people to use it?

Getting young people to use a product is bloody hard. But the future of Kooth pretty much relies on it. If Kooth don’t get enough young people to use their app, the economics of the contract will look poor. Someone will divide the cost by the number of users, and if that number is too high, Kooth will be under pressure.

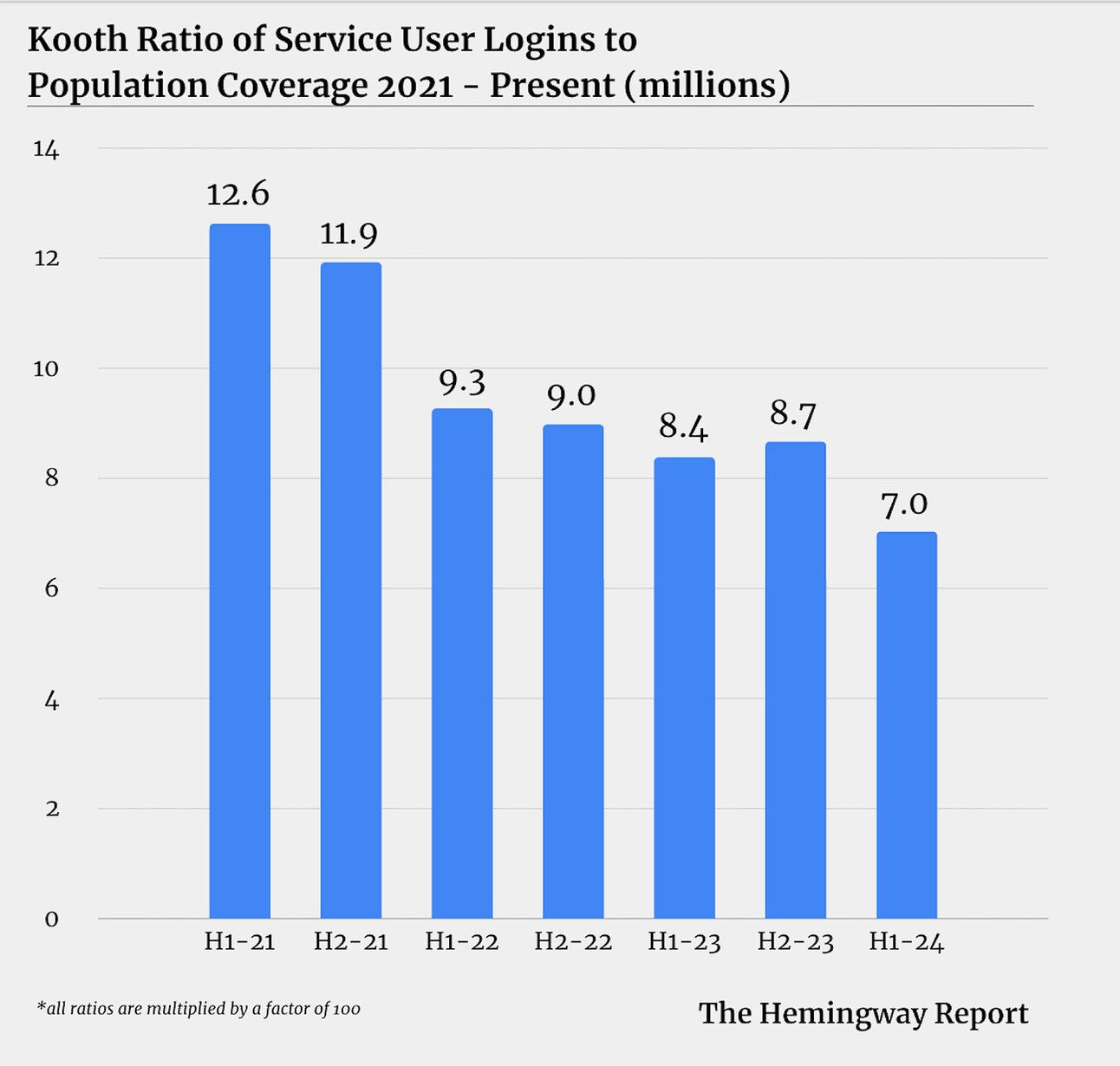

How are they doing so far?

While they don’t share much user data (e.g., Monthly Active Users), they do share “service logins" - how many times people have logged into their app. This has been essentially flat over the past few years.

This is despite increases in the size of the population they are covered to serve.

Essentially, the penetration of their product relative to the size of their covered populations has been decreasing.

I will admit that I can’t know enough with the data I have, to know if this is an issue for Kooth or not. They could be ramping down efforts for certain contracts which is leading to lower usage. Plus, the California contract is still getting off the ground.

But either way, reaching young people and driving product usage must be a major priority.

(a) Reaching young people:

A recent investor deck gives us some insight into how Kooth thinks about reaching young people. They have three channels;

- Reaching them through schools and universities (Education)

- Reaching them through healthcare services

- Reaching them directly through social media and search

The first two rely on working with partner organisations whilst the third is Kooth going direct to users.

Both have their challenges.

Partner organisations

Kooth can work with the organisations who already have relationships with young people - primarily schools and community mental health services. Kooth have had a lot of success getting these organisations to refer young people to their product.

But the challenge here is that it’s a constant battle to get enough organisations continuously talking about you and referring enough young people to sustain user growth. It’s just not their core incentive and they have other things to worry about each day (like running a school). There’s a bunch of stuff you can do to encourage referrals and keep your product top of mind, but it’s hard - read about the challenges of partnerships in mental health here.

Going direct. In this channel, Kooth take the primary responsibility for reaching young people and getting them to download their app. To do this, they are investing in social content on instagram and TikTok - but their reach is so far pretty minimal. Just this week they announced an initiative partnering with creators and influencers to help young people develop content creation skills and talk about mental health. I would guess this is a play to generate a bunch of social content but also think it is more UK focused. They don’t seem to be running any social ads.

Going direct is hard and it’s expensive. Kooth have no presence or brand reputation in California. It will be an uphill battle to acquire enough users to justify the value of this contract.

It’s hard to know how Kooth are doing so far with driving usage. The Google Play store shows Soluna having over 50k downloads with the Apple Store looking somewhere around the same. Around 100,000 downloads isn’t bad considering it was only launched in January. But the challenge will be justifying that against the cost of the contract.

If we estimate the cost of this California contract to be around $40m a year, we could get a cost per download of approximately of $400.

But that’s just the cost to get people to download the app. Getting young people to actually use it is a different story.

(b) Getting young people to use it

How many apps do you actually use each week? Only a handful right? When’s the last time you download a new app and consistently use it?

It’s really hard to get people to use an app on an ongoing basis.

There are teams of very smart people in silicon valley who spend every day thinking about this problem. Their apps are often built to be purposefully addictive to kids, and even these guys fail a lot of the time to get young people to use their app.

A lot of the outcomes from digital mental health solutions are dependent on continued usage and adherence but achieving that adherence, especially with young people is very difficult.

I don’t know what Kooth’s engagement and retention metrics are but I would guess it’s a constant topic of conversation for their product team and it’s definitely something they will need to get right if they are going to deliver on the value of their California contract.

2. Can they deliver outcomes (and prove it)?

Of course, this contract will ultimately be evaluated by the outcomes it delivers for young people in California. Kooth have good evidence that their product can deliver positive outcomes in both prevention and early intervention for patients but also in cost savings to the health system.

But this contract is for a new population of young people from a wide range of backgrounds and cultural contexts. Will their product efficacy hold up in California and can they generate the evidence that proves their value? I certainly hope so, but it will require a big effort from the Kooth team.

Kooth have got their chance.

They’ve been handed the QB1 jersey and given their shot at the big time. If they spend the next couple of years throwing touchdowns across the state of California, then their potential to expand around the US is huge. But throw a few interceptions and they could quickly find themselves back on the bench, ruing their missed opportunity.

The balls in their hands.

Football puns over…

5. Expectations

So what can we expect for Kooth?

As you’ve probably guessed, there’s a bull and bear case, divided by their potential performance in Calirofnia.

The bull case:

The bull case for Kooth is that their California contract exceeds expectations. They can get people to download and use the app and deliver significant outcomes for them. They can show this to the state and demonstrate the return and associated cost savings. If that is the case, they can use that traction to expand into more pilots and contracts with States and other funders across the US. If they can maintain their gross margins whilst doing this, it could be a serious business with the potential to generate hundreds of millions in revenue and tens of millions in net profit.

The bear case:

The bear case, is that the California contract doesn’t go to plan and it hinders their ability to expand across the US. If you fail to deliver on a $180 million dollar contract I’m just not sure how you can come back from that and convince the next payer it will be different for them.

I like Kooth. I like their dedication to youth mental health. I like their product. I like how long they have been around for and the slow and steady approach they have taken to mindfully building their business.

Yes, it’s going to be a touch challenge. But that’s the game we are playing. This is a massive problem and we need people willing to take on tough challenges like this.

Kooth have a huge opportunity to improve the lives of young people across the US, UK and abroad and I’ll be rooting for them every step of the way!

That’s all for this week.

If you liked this post, the best thing you can do is to share it with someone else. It would mean a lot.

Keep fighting the good fight!

Steve

Founder of The Hemingway Group

P.S. feel free to connect with me on LinkedIn