#2 Pear-Shaped: How the darling of digital therapeutics raised $400m and then went bankrupt.

A case study on Pear Therapeutics, an AI business supporting blended care, and all this week's latest mental health news and job openings.

Hi friends,

There’s one question that’s been on my mind for over a year now.

What the hell happened to Pear Therapeutics?

They were once the darling of the mental health startup world before going out in a ball of flames. But why??

This week, I finally got an answer to it and wrote 2,500 words explaining everything I learned… It’s a lot, I know, but I promise you it’s worth it.

The good news is I had a bunch of fun doing it too. Looks like deciding to write The Hemingway Report was a good idea after all and I hope you enjoy reading it as much as I enjoyed writing it.

Before we dive into this week’s content…I’d love to hear what you think of The Hemingway Report.

So please reply to this email with your thoughts. The reason I write it is to be helpful to people like you, so please tell me what you enjoy and what you’d like more of. It would be incredibly helpful.This week in The Hemingway Report:

- Pear-Shaped: How Pear Therapeutics went bankrupt after raising $400m (and what we can learn from them)

- Limbic AI: the London based company using AI to deliver blended care

- Profitability (finally): Talkspace reaches profitability after shifting focus to B2B model

- Jobs: open positions at the top mental health businesses

Pear-Shaped, how Pear Therapeutics raised $400m and went bankrupt 2 years later.

If you pitch your mental health startup to an investor, there’s one question they are all likely to ask you…

“How do I know you won’t end up like Pear Therapeutics?”

In 2021, Pear Therapeutics was the darling of the mental health startup world. They developed a suite of digital therapeutics, got them FDA approved, partnered with industry giants, raised over $400m form top investors and even went public.

But in 2023, they filed for bankruptcy.

Every time I talk with a mental health founder, this question comes up as we try to understand what went wrong for this business. After months of research, I finally have a good answer.

Now, let me be clear.. this is not a hit piece.

Having worked at two high growth startups, I know how hard it is to try and build a big business.

Most days, you’re just trying to keep your head above water. It’s the easiest thing in the world for commentators on the sideline to point out what you should have done differently. So I actually commend the Pear founders, executives and team. They tried something new. They broke new ground - becoming one of the first organisations to receive authorisation from the FDA to market prescription digital therapeutics (PDTs) for mental health disorders - and paved the way for the PDT category.

Sure, it didn’t work out, but they gave it a hell of a crack and that’s what matters.

The purpose of this article is not to criticise them, but rather to see what we can learn from this story, so that future founders might avoid the mistakes that led to this business’s untimely death.

Now, if you don’t know who Pear Therapeutics are, let me fill you in….

At the core of Pear’s founding story, was the belief that Prescription Digital Therapeutics were going to be a new class of medicines. Specifically, they believed that building evidence based mobile apps which complemented clinical visits and existing treatments for mental disorders, could improve mental health outcomes.

They started by building reSET, a CBT based mobile app, aimed at treating patients with substance use disorder. reSET consisted of a twelve week program comprising sixty two interactive modules and in 2017, they received FDA approval to market reSET as a digital therapeutic.

In 2018, the FDA approved a follow-up app, reSET-O, focused on treating patients with opioid use disorder through two major behavioural therapy approaches, buprenorphine and contingency management.

Then in 2020, they launched Somryst aimed at treating insomnia (CBT-I) over nine weeks with six core treatment modules and a sleep diary feature.

On the product development side, they were doing a lot right. They were tackling big categories (substance use disorders and insomnia), built products that demonstrated good results and did the hard work of getting them approved by the FDA.

Abstinence rates of patients who used reSET (excluding those primarily suffering from opioid use disorder) more than doubled. Retention of patients with opioid use disorder who used reSET-O increased by almost 15% and more than 40% of patients who used Somryst no longer met the criteria for insomnia upon completion of the program.

Pear's results were promising, and so was their future.

By this stage (June 2020) they had already raised $409m across eight rounds from investors such as Softbank Vision Fund, Temasek Holdings and Novartis.

Now, cast yourself back to 2021 for a moment. Tech valuations were soaring and SPACs (Special Purpose Acquisition Companies) were all the rage. Pear was no exception from the trends.

In March 2021, Pear Therapeutics went public via SPAC at a valuation of US$1.6B - a whopping four hundred times their 2021 revenue!

But just twenty four months later, Pear filed for bankruptcy.

Now, excuse me while I state the extremely obvious…

Pear went bankrupt because they ran out of money.

In fact, that’s pretty much the only way you can go bankrupt. But considering they had taken in over $400m of investor cash, how did they run out of it all?

It boils down to three things – they failed to commercialise their existing products, they created an unsustainable cost base and they over-invested in R&D.

Let’s break each of those down.

1. Failure to commercialise

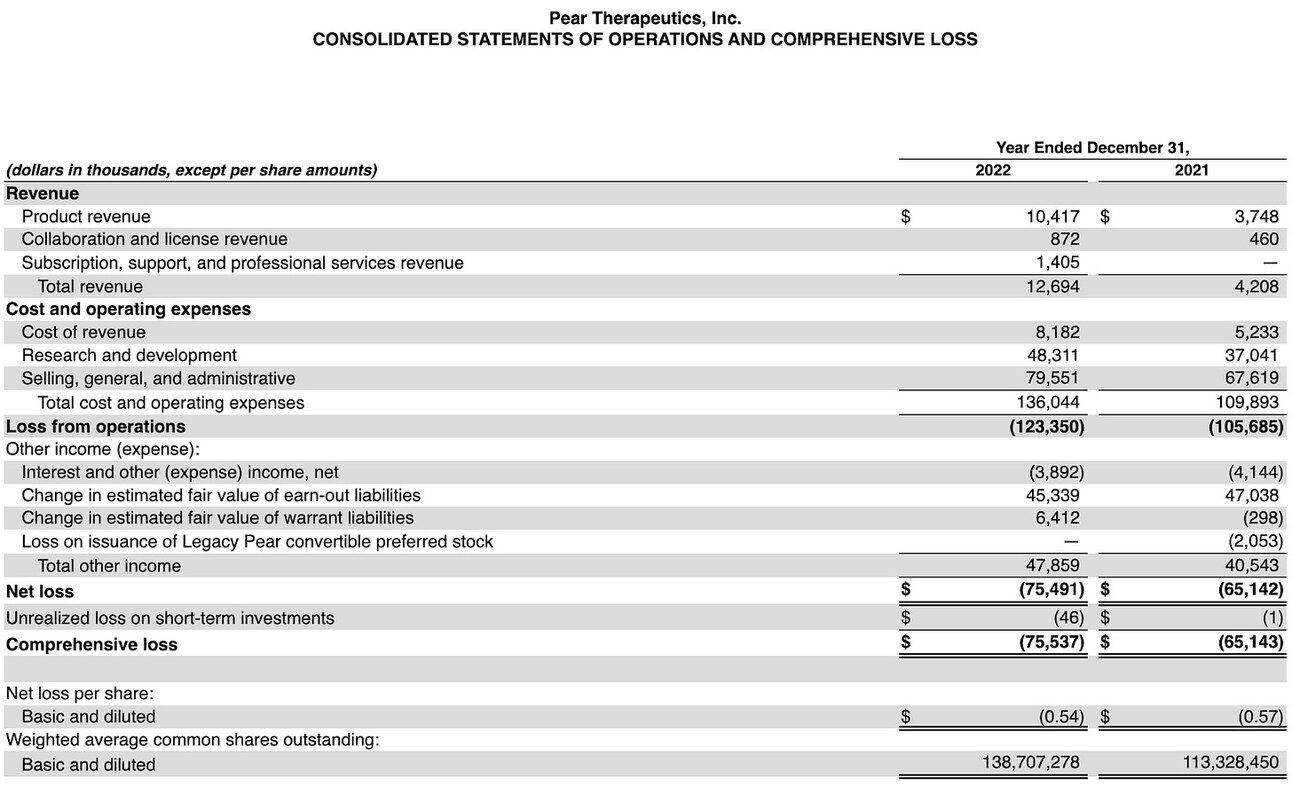

In 2022, Pear had three FDA approved products suitable for tens of millions of people in the US. But they only made $10 million in revenue.

For Pear to make revenue, three things had to happen;

- A clinician had to prescribe their product to a patient

- The patient had to fulfil that prescription (i.e., download the app)

- Pear had to get paid for this prescription (usually by being reimbursed by a payor)

The problem for Pear was that this revenue funnel was full of leaks. In the first nine months of 2022, 31,000 prescriptions were written for Pear’s products. But only 58% of these prescriptions were filled and Pear Therapeutics were paid for only 41% of those fulfilled prescriptions.

So for every four prescriptions written, Pear were only paid for one.

Increase the percentage of prescriptions that get filled is largely a user experience and marketing problem. If a patient gets prescribed a treatment, what would stop them from fulfilling it? Either they think it won’t work (we know this is a barrier for a lot of mental health treatments), practically fulfilling the prescription is hard (there’s friction in downloading or accessing the product) or the cost is too high / it’s not reimbursable.

Increasing reimbursement is a matter of getting more payors on board. If you work in healthcare, this is what keeps you up at night. This require massive amounts of relationship building, sales work and evidence to convince them to support your product.

Successful commercialisation of these products would also have required much stronger adoption by clinicians.

They are the ones who hold the pen on the treatments they prescribe. Getting clinicians on board is another notoriously difficult part of working in healthcare. You have to go clinician to clinician, and convince them that this is good for their patients and good for them. Now we don’t know exactly why more clinicians were not prescribing Pear products, but we do know that healthcare professionals are notoriously slow to adopt new technologies. So this was both a market wide problem AND a Pear problem. Either way, they couldn’t figure out how to get more clinicians prescribing their products at scale.

So we can start to see just how hard a task Pear had on it’s hands….

They had to convince payors to reimburse their product, clinicians to prescribe it and users to use it.

Doing just one of these things is a mammoth task for a startup. Doing all three is gargantuan.

Turns out, startups are freaking hard…

So what could they have done instead?

Instead of equally focusing on all three segments, what if they just focused on clinicians? Could they have spent all their effort convincing them that this product is truly fantastic and use that drive prescription numbers? This would drive the top of their revenue funnel (the number of prescriptions) - which is, from a mathematical perspective uncapped, compared to optimising conversion rates through a funnel.

This wouldn't fix their fulfilment problem, but you have to make tradeoffs in startups, and this was one that could have been worth it. Large prescription numbers could then be used to further convince payors to support the treatment. Of course, there’s a chicken and egg element to this. Clinicians are unlikely to prescribe something if they know it is not reimbursable… That’s what makes this space so tricky!

Fixing 100% of these leaks in their funnel (completely unrealistic) would certainly have helped their case, quadrupling their revenue, but it would still have delivered only $40m of income - nowhere near enough to support the $136m in operating expenses they incurred in 2021.

So Pear had a revenue problem. But a lack of revenue doesn’t necessarily put an organisation out of business. If Pear had only been spending $20m a year, they would have had another 6 years of runway from 2021… But that was not the case.

2. An unsustainable cost base

Pear had developed a ginormous operating cost base.

Like, $136m ginormous…

So what were they spending this money on?

$80m of it was spent on SG&A expenses.

Essentially, Pear went on a hiring spree and brought in a tonne of people to try to drive adoption of their products. They call this out in their 2022 10-K “SG&A expenses consist primarily of compensation for personnel, including stock-based compensation related to commercial, marketing, executive [and other] functions”.

Pear were not alone in doing this during the 2020 - 2022 boom. Lots of tech companies over-hired. But it doesn’t make for pretty viewing. I think the lesson here is that before you have a predictable growth model, headcount does not translate directly to revenue.

Take a successful Series B SAAS company for example, one that has proven their Go To Market model and have built a predictable growth model. They know how to acquire leads and convert them to customers. They know the cost to do this and the rates at which they convert.

So that means they can say with decent confidence that if they increase the flow of leads into the top of this funnel (by investing more in their acquisition channels) and converting these leads (by hiring more sales people), then revenue will also increase.

Of course, SAAS companies still get this wrong, but at least the maths makes sense. It’s something you can put in an excel model with reasonable accuracy.

But if you don’t have a proven GTM model (which Pear didn’t), then investing significantly more in sales and marketing is a massive risk. It’s a “we’ll hopefully figure it out” investment as opposed to a “we are accelerating something that we know works” investment.

And if you’re investing $80m into it every year, you better make damn sure it’s the second kind of investment.

Many problems in the startup world can be solved with brute force. But others actually require strategy. They require deep thinking from the exec team and for them to come up with clever solutions (before turning to brute force).

The only thing riskier than investing in sales and marketing without a proven GTM model, is investing in more products before you can commercialise the ones you already have.

Unfortunately, Pear did this too.

3. Over-investment in R&D

This is Pear’s product pipeline in 2022. Fourteen different products.

This is great news if you have a clear way to make money from these once they are proven, approved and brought to market. But they didn’t!

Unfortunately these products never made it to market. But if they had, it’s likely they would have met the same commercial challenges of reSET, reSET-O and Somryst.

What also strikes me here is the breadth of categories they were going after, branching outside of psychiatry to neurology and even other areas like oncology and cardiovascular disease.

I’m delighted to see they were making progress on these important areas, but I would love to know what their plan was here.

Each of these products would have needed an entirely new Go To Market and commercial strategy. So even if they cracked commercialisation with their psychiatry products, they would have had to start from scratch for these new products as they brought them to market.

The reason this pipeline contributed to killing Pear, is that it was super expensive to build. In 2022, they spent $48m on R&D alone.

Pear spent $80m on SG&A, $48m on R&D, while only making $10.4m in revenue in 2022… it doesn’t take a genius to see why they were in trouble.

They tried to stem the died, conducting two rounds of layoffs in 2022, but it was too little too late. In April 2023, they filed for bankruptcy.

I’ve been thinking about what the root cause of Pear’s issues were.

One hypothesis is that their VCs pushed them to invest heavily in order to drive their growth. I know what this is like, VCs want the massive outcome and most get impatient with slow results, so they tell you to be aggressive, to scale faster, hire more (at least this is what they were all saying in 2021, funnily enough many of them changed their tune pretty quickly once the markets turned…).

With investors like SoftBank on their cap table, I am sure there was an element of this pressure. Now, I could write a whole article on this dynamic, including when it’s right to “go for broke” vs when it’s not.

But ultimately it boils down to whether or not you are in a winner-takes-all market AND if there’s an advantage to being first. This is usually a market where there are economies of scale or large network effects. In these markets, a race to be first by investing aggressively, can be justified.

But the digital therapeutics market has neither of these traits.

So what can we learn from Pear?

Ignore commercialisation at your peril. Pear built great products but just couldn’t generate revenue from them. They never cracked their Go To Market model and couldn’t convince enough clinicians, payors and patients to adopt their products. If you still believe in the “build it and they will come” maxim, hopefully this convinces you of its falsehood. Building a successful mental health startup requires clinical, scientific and product genius. But it also requires commercial genius. It needs people capable of defining a successful Go To Market strategy so you can acquire clinicians, payors and users, predictably and at a sustainable cost.

Keep your costs in check. This is so basic I nearly didn’t include it… but please, keep a handle on your expenses. Spending eight times your revenue on SG&A is like driving down a country road at 200km/hr and then wondering why you’re suddenly upside down in the ditch. You only have to quit when you run out of money. Having a low operating cost base buys you time, and in this market, time is crucial.

Nail one product before investing in more. Pear invested massive money into developing a suite of new products before they could even make money off one. It’s tempting to turn your attention towards new products, hoping that the next one will also solve your commercialisation issues. But hope is not a strategy. If you’ve got a product in the market, make sure you are able to make money off it before you build a massive pipeline of future products.

Being first is hard. Pear were a trailblazer in the digital therapeutics market, but that meant they also had to create the category. When trying to convince clinicians, payors or patients, they didn’t just have to convince them that the Pear products were a good idea, they had to convince them that the whole category of Digital Therapeutics was a good idea. That’s a bloody hard thing to do and few can pull it off. They’ve done a lot of heavy lifting for the DT category, paving the road for the next batch of companies to get FDA approved and adopted. Unfortunately however, none of that benefit will accrue to Pear. Sometimes being second is easier than being first!

I admire Pear. They had a vision and were bold about pursuing it.

They made decisions that were not abnormal for the time they were in, but that sadly, led to their demise. I’m hopeful about Digital Therapeutics as a category and am grateful to Pear for being the first ones to pave the road for future companies in this space.

I’d love to hear your thoughts on Pear and if you found this helpful. Shoot me a reply to tell me what you think.

Mental Health News

Here’s your roundup of the top news in mental health this week;

- Tava Health raises $20m to expand their mental healthcare platform (GlobalData)

- Private Equity now owns 6.2% of mental health treatment facilities in the US (BHBusiness)

- Nasdaq-listed online therapy provider Talkspace is finally profitable, proving shift from D2C to B2B model to be successful (BHBusiness)

- Backpack Healthcare, a US-based paediatric mental health provider, raises US$14 million in Series A funding (BHBusiness)

- Medibank’s Amplar Health and Aurora Healthcare collaborate to form iMH, set to open new mental health hospital with 58 beds in Brisbane (Insurance Business Mag)

Company Spotlight: Limbic AI

- What they do: provide clinical AI tools to enhance mental healthcare services, focusing on assessment and providing support to patients in between therapy sessions.

- Headquarters: London, UK

- Founders: Ross Harper and Sebastian de Vries

- Founded: 2018

Limbic’s strategy is based on the fact that we just don’t have enough clinicians to meet the demand for mental health services. They build software to support clinicians in delivering care and have two main products;

Limbic Access is a chatbot that acts as a digital front door for services. It allows patients to self-refer and also conducts initial assessment. This both improves patient experience and saves time for clinicians.

Limbic Care is a chat-based tool for patients to interact with in between their therapy sessions. They can complete activities and review content aligned with their treatment plan. Clinicians have control over the content their patients see and are also alerted by Limbic is any high risk behaviour is identified.

Limbic has had great traction with the NHS so far and in March of this year, raised $14m from Khosla Ventures. They are another great example of a company supporting a blended model of care for patients, a trend I’m very excited to follow in the coming years.

Jobs

- Career Development Research Fellow in Cognitive Psychology/Cognitive Neuroscience @ Oxford University for OPM-MEG, a neuroimaging technology (Role description) (More information)

- Healthtech Sales Specialist @ Updoc (LinkedIn)

- Director Commercialisation (Social and Behavioural Sciences) @ UniQuest (Startmate)

- Partnerships Manager @ Like Family (LinkedIn)

- Associate Lecturer, Psychology @ University of New South Wales (LinkedIn)

- Research Associate / Senior Research Associate in NSW Child Development Study @ University of New South Wales (LinkedIn)

- Lecturer in Mental Health @ Flinders University (LinkedIn)

- Various @ Headway (Accel)

Make it this far? Fair play! Reply to this email and let me know what you thought.

That’s all for this week.

Keep fighting the good fight!

Steve Duke

Founder of The Hemingway Group

P.S. feel free to connect with me on LinkedIn

Like this post? Feel free to share it. It would mean a lot.